[Exclusive] 56 Trillion Won Jisan Loans Trigger 'Warning Light'... Bank NPL Ratio Surpasses 1% for First Time

Sixteen Korean Banks Near 56 Trillion Won in Jisan Exposure

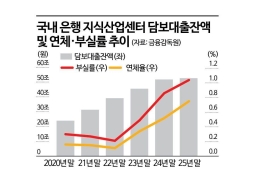

Collateralized Loans Reach 52.6 Trillion Won, Doubling in Five Years

IBK at 13.2 Trillion Won, KB at 11.5 Trillion Won... Delinquency Rate at 0.75%, Default Rate at 1.04%

Jisan Ris

The scale of collateralized loans extended by banks for knowledge industry centers (so-called 'Jisan'), which are struggling with vacancy and unsold units, reached 53 trillion won as of the end of last year, with the delinquency ratio surpassing 1% for the first time. The risk of banks suffering further losses is growing, compounded by a surge in auctioned properties and a sharp drop in successful bid rates, after banks aggressively increased Jisan lending in the wake of COVID-19. While some believe the worst phase has passed thanks to risk management measures adopted by banks over the past two to three years, there are concerns that accumulated risks, due to external variables such as delayed economic recovery and the possibility of prolonged high interest rates triggered by the Middle East, could weigh on banks' financial health for an extended period.

Jisan Collateralized Loans Double in Five Years... Delinquency Rate at 0.75%, Non-Performing Loan Ratio at 1.04%

![[Exclusive] 56 Trillion Won Jisan Loans Trigger 'Warning Light'... Bank NPL Ratio Surpasses 1% for First Time](http://www.asiae.co.kr/news/img_view.htm?img=2026042910474645176_1777427266.jpg)

According to data submitted by Assemblyman Yoon Han-hong of the People Power Party to the Financial Supervisory Service on April 29, the outstanding balance of Jisan collateralized loans at 16 domestic banks amounted to 52.6 trillion won at the end of last year. This is more than double the amount from the end of 2020 (23.9 trillion won) in just five years. Adding interim payment loans (1.3 trillion won) and project financing (PF) loans (1.9 trillion won), the total Jisan exposure stands at 55.9 trillion won.

By bank, IBK Industrial Bank of Korea had the largest outstanding Jisan collateralized loan balance at 13.19 trillion won, followed by KB Kookmin Bank (11.54 trillion won), and NH Nonghyup Bank (8.38 trillion won). Shinhan Bank (6.36 trillion won), Hana Bank (5.92 trillion won), and Woori Bank (5.72 trillion won) followed in that order.

Key asset quality indicators are deteriorating rapidly. The average non-performing loan (NPL) ratio (delinquent over 90 days) for Jisan collateralized loans rose from 0.3% at the end of 2020 to 0.86% at the end of 2024, and climbed to 1.04% at the end of 2025, exceeding 1% for the first time. In response, the Financial Supervisory Service convened major bank loan policy officers last month to conduct a close review of the Jisan loan situation, ordering the submission of management plans and strengthening of loan loss provision reserves. By bank, IBK Industrial Bank of Korea posted the highest NPL ratio at 1.64%, the highest among banks with balances exceeding several hundred billion won, excluding SC First Bank and Suhyup Bank with much smaller balances. Hana Bank followed with 0.97%, then Shinhan Bank (0.9%), Kookmin Bank (0.87%), and Nonghyup Bank (0.82%), while Woori Bank had a comparatively lower ratio at 0.52%.

The average delinquency rate (over 30 days past due) stood at 0.75% at the end of 2025, higher than the corporate loan delinquency rate for domestic banks at the same point (0.59%). This suggests that risk in Jisan lending is increasing faster than in general corporate loans. SC First Bank had the highest delinquency rate at 3.1%, while IBK Industrial Bank of Korea recorded 1.1%. The remaining five major commercial banks all recorded less than 1%. For Jisan interim payment loans, the outstanding balance has dropped to the 1 trillion won range, but the average delinquency rate as of the end of last year stood at 9.95%, highlighting the seriousness of the situation.

Jisan, known as 'apartment-type factories,' saw a surge in supply in 2020 as they were sought out as investment destinations to avoid low interest rates and lending regulations during the onset of COVID-19. At the time, banks rapidly increased lending, applying loan-to-value (LTV) ratios as high as 70-80%. However, the situation changed dramatically with interest rate hikes and economic slowdown. As tenant companies go out of business and vacancies rise, rental income has dried up, and allottees are simultaneously burdened with management fees and interest payments, rapidly eroding their repayment capacity. According to the Korea Research Institute of Real Estate Development Industry, the Jisan vacancy rate in the Seoul metropolitan area soared to 55% in February this year. Analysts point out that shrinking demand for occupancy is accelerating the expansion of non-performing loans. Consequently, the number of auctioned properties more than doubled to 1,576 in the first quarter of this year compared to the same period last year (625), and the successful bid rate plummeted from 61.63% to 52.5% in the same period.

![[Exclusive] 56 Trillion Won Jisan Loans Trigger 'Warning Light'... Bank NPL Ratio Surpasses 1% for First Time](http://www.asiae.co.kr/news/img_view.htm?img=2026042910405045151_1777426850.jpg)

Despite Tightened Lending, Non-Performing Loans Expected to Continue Rising Amid Prolonged High Interest Rates

Banks have already begun strengthening loan management. Since the downturn in 2023, new Jisan lending has been virtually halted, with lower LTVs and much stricter screening applied to loan extensions. As a result, more borrowers are complaining about a 'loan cliff' due to difficulties in securing funds. An official at one major commercial bank explained, "Since last year, we have lowered the LTV for Jisan loans, reducing loan limits. For properties with a history of long-term vacancies, we now require pre-loan inspections and head office reviews for new loans." The official added, "We are also strengthening screening by requiring the submission of bank transaction records to verify whether rental income is being properly collected."

The key issue is the 'exit strategy.' For banks with large Jisan loan portfolios and high NPL ratios, rapidly recalling loans could instantly materialize bad debts, further reducing asset values and recovery rates. It is reported that recent recovery rates on real estate-related non-performing loan sales are around 70% in Seoul and 50% in non-metropolitan regions. Another bank official noted, "In a situation with no rental income due to vacancies, sharply reducing loans makes it tough for borrowers to survive, ultimately leading to more bad loans. It is difficult to strike a balance between risk management and market stability."

The possibility of further expansion of Jisan non-performing loans cannot be ruled out. If the environment of high oil prices, high exchange rates, and high interest rates—the so-called 'triple high'—continues, recovery in occupancy demand and improvements in borrower repayment capacity may be delayed. Although the government is proposing measures such as expanding eligible industries for occupancy and public purchases, it is likely that the effects will be limited to prime locations, meaning it will take considerable time to resolve vacancies across the board. A financial industry official said, "Although risks are being addressed due to banks' tighter management, the continued rise in both delinquency and NPL ratios means aftershocks will persist for some time."

Hot Picks Today

![Home Appliance Woes Mount, Yet 45 Trillion Won in Bonuses? Samsung's Risky Asymmetry [Why&Next]](https://cwcontent.asiae.co.kr/asiaresize/93/2022111609212518207_1668558086.jpg) Home Appliance Woes Mount, Yet 45 Trillion Won ...

Home Appliance Woes Mount, Yet 45 Trillion Won ...

- "Major Crash Is Coming... Buy Even If You Have to Skip a Meal" 'Rich Dad' Shares...

- Man Suspected of Illegal Filming in Women's Restroom Boldly Says "Conduct Forens...

- 500% Energy Efficiency... Samsung Electronics’ 'Energy Magic' to End the Fear o...

- "It Was Fantastic" Jensen Huang's Daughter Seals 'Robot Alliance' with LG throug...

An official at the Financial Supervisory Service commented, "While current asset quality indicators for Jisan loans are not at a very severe level, ongoing monitoring is needed as risks may increase depending on external variables such as the Middle East situation."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.