[1mm Finance Talk] Alarming Signs Behind Record Profits... Banks' NPLs Surge by 11%

Despite Record 3.8 Trillion Won in First-Quarter Profits for Major Banks,

Asset Quality Indicators Worsen: NPLs and Delinquency Rates on the Rise

Increase in Bad Loans, Especially Among SMEs

Expansion of Productive Finance and K-Shaped Grow

The asset quality indicators of the four major domestic banks deteriorated across the board in the first quarter of this year. Non-performing loans increased by 11% in just three months, and the delinquency rate surged, heightening concerns about additional bad debt. Experts note that the increase in non-performing loans among small and medium-sized enterprises (SMEs) is particularly notable, as banks compete to expand productive finance amidst deepening economic polarization and the prolonged war in Iran.

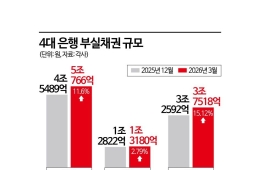

According to the financial sector on April 29, the combined non-performing loans (NPLs) of the four major commercial banks (KB Kookmin, Shinhan, Hana, and Woori) stood at 5.0766 trillion won as of the end of March 2026. This represents an increase of 11.6% (527.7 billion won) compared to the end of last year, marking a steep upward trend. As a result, the NPL ratio—non-performing loans as a percentage of total won-denominated loans—increased from 0.31% to 0.34%.

![[1mm Finance Talk] Alarming Signs Behind Record Profits... Banks' NPLs Surge by 11%](http://www.asiae.co.kr/news/img_view.htm?img=2026042811420643457_1777344126.jpg)

Banks classify loans as non-performing when borrowers fail to repay principal or interest for more than three months. Non-performing loans increased to 4.9 trillion won at the end of June last year, then the growth slowed to 4.8763 trillion won at the end of September, and further declined to 4.5489 trillion won by year-end. However, since the beginning of this year, non-performing loans have risen again, and the quarter-over-quarter increase is the highest since March 2025 (22%).

The rise in non-performing loans was largely driven by corporate loan defaults. As of the first quarter, the volume of non-performing corporate loans reached 3.7518 trillion won, up 15.12% (492.7 billion won) from the end of last year. While household non-performing loans also increased to 1.318 trillion won, the growth rate was limited to 2.79% during the same period.

This suggests that while macroeconomic indicators such as GDP growth and the current account balance, especially in the semiconductor sector, are improving, the real economy—including SMEs—remains sluggish. As banks have competitively expanded productive finance, they may have relatively neglected the management of asset quality indicators. Additionally, following the real estate project financing (PF) crisis, the market for selling and writing off non-performing loans has frozen, making banks less proactive in disposing of bad debt, which is also cited as a key reason for the increase in non-performing loans.

The pressing issue is that non-performing loans may continue to rise. The average delinquency rate of the four major banks—loans overdue by more than one month in principal or interest—increased from 0.31% at the end of last year to 0.36% at the end of March 2026.

![[1mm Finance Talk] Alarming Signs Behind Record Profits... Banks' NPLs Surge by 11%](http://www.asiae.co.kr/news/img_view.htm?img=2026042811420543456_1777344125.jpg)

Among these, the corporate loan delinquency rate rose from 0.34% to 0.42%, outpacing the overall rate of increase. By company size, large corporations maintained a stable rate (0.12%), while the SME delinquency rate climbed from 0.45% to 0.54% in just three months—a 0.09 percentage point rise. Notably, Hana Bank (0.64%) and Woori Bank (0.61%) posted SME delinquency rates above 0.6%, the highest since 2019. Meanwhile, delinquency rates for household loans also reversed to an upward trend at all four banks within three to four quarters, signaling ongoing risk.

Given that loans overdue for more than three months are classified as non-performing, non-performing loans are likely to increase further in the coming months. Despite the four major banks posting a record net profit of 3.8843 trillion won in the first quarter, they are now facing a structural crisis of worsening asset quality beneath the surface.

Although banks are proactively setting aside loan-loss provisions to manage bad debt, the pace of new non-performing loans is outstripping these efforts. Banks that set aside relatively fewer provisions in the first quarter may need to expand their reserves further from the second quarter onward. In fact, Hana Bank, which ranked second in net income in the first quarter, indicated during a recent conference call that loan-loss costs may rise from the second quarter.

Hot Picks Today

![Benefiting from Non-Chinese Demand and SpaceX News, This Stock Surged 257%... How Long Will the Rally Last? [This Week's Hot Stock]](https://cwcontent.asiae.co.kr/asiaresize/93/2025081909273687512_1755563255.jpg) Benefiting from Non-Chinese Demand and SpaceX N...

Benefiting from Non-Chinese Demand and SpaceX N...

- Gangneung Hotels Jump from 80,000 Won to Over 600,000 Won... Korea, China, Japan...

- "You'll Regret Not Buying Now"... Minister Urges Travelers to Purchase Airline T...

- Stock Market Soars, but Private Equity Fund Managers Retreat

- 'Maternity Leave for Second Child' Interrupted... 1997-born White House Spokespe...

An industry insider commented, "While banks are under pressure to expand productive finance, the added geopolitical risks in the Middle East could further weaken the repayment capacity of SMEs and self-employed individuals, which we are closely monitoring." The insider added, "We are facing a deepening dilemma between proactive asset quality management and the expansion of productive finance."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.