AI-Driven Memory Semiconductor Super Boom...Exports Surge 173%

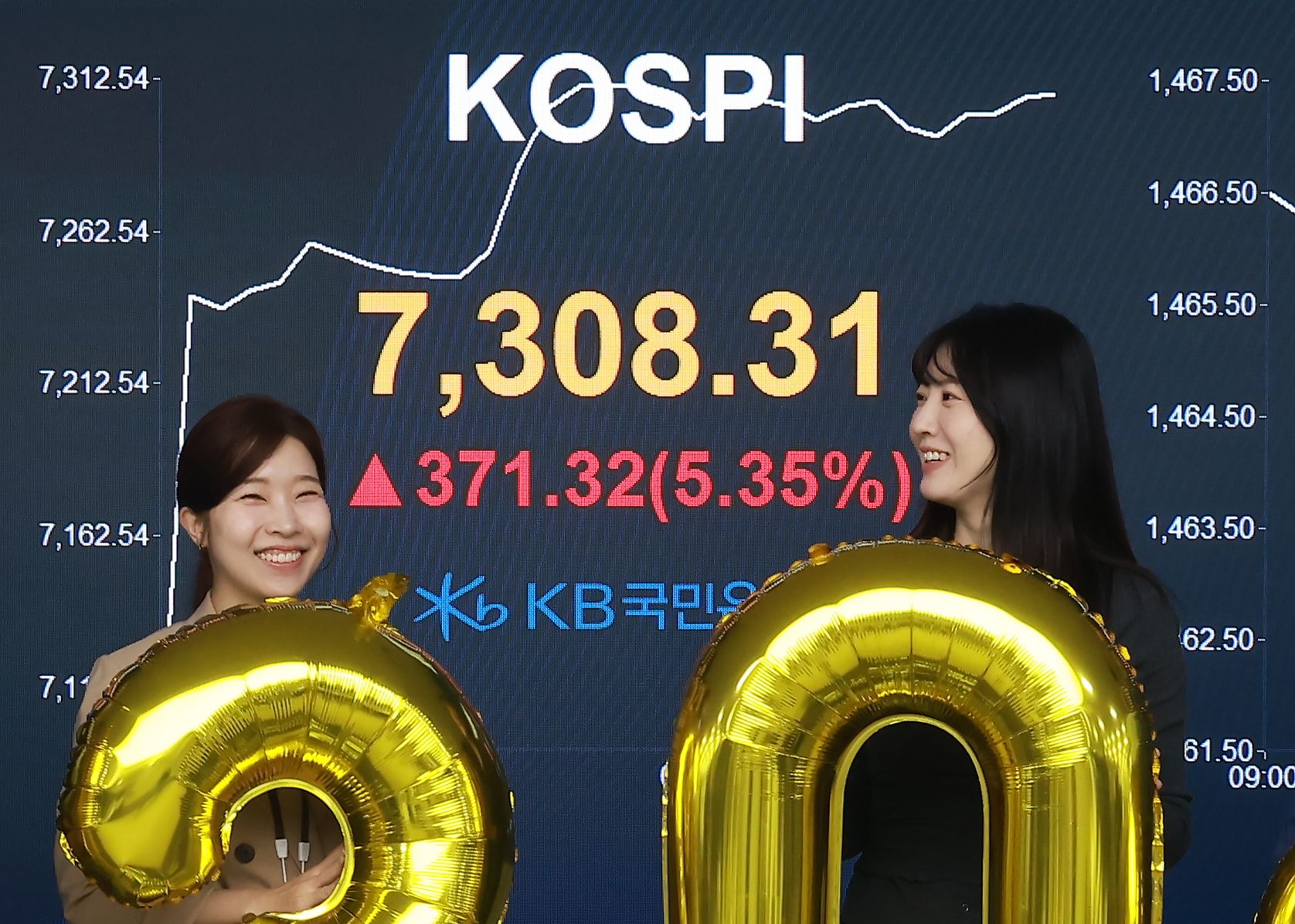

The KOSPI has finally reached the long-awaited “7,000-point mark,” setting a new chapter in the history of the Korean stock market. This milestone comes as Korean companies emerge as key beneficiaries amid the sweeping changes brought on by the artificial intelligence (AI) revolution. Market experts believe the current memory semiconductor super boom will continue into next year, making it highly likely that the KOSPI could even reach 8,000 points.

KOSPI Surpasses 7,000 for the First Time Ever... Forecasts for 8,000 Abound

According to the financial investment industry on May 6, despite the ongoing conflict between the United States and Iran and the continued high international oil prices, the stock market has climbed thanks to the explosive demand for AI-driven memory semiconductors. According to the Ministry of Trade, Industry and Energy, Korea’s semiconductor exports last month surged 173.5% year-on-year to reach $31.9 billion. This figure is second only to the record $32.8 billion posted in March, making it the second-highest monthly export total ever. For 13 consecutive months, semiconductors have set new monthly records for exports.

DDR5 and HBM Price Explosion, Key Drivers of KOSPI Rise

Samsung Electronics and SK Hynix Account for 90% of Profit Increase

The expansion of AI server investments has caused prices for advanced memory semiconductors such as high bandwidth memory (HBM), DDR5, and NAND flash to skyrocket, resulting in a surge in exports. Compared to one year ago, fixed memory prices have soared: DDR4 8Gb by 870%, DDR5 16Gb by 662%, and NAND 128Gb by 766%, pushing up the overall export value. The Export-Import Bank of Korea expects that, boosted by the semiconductor super boom, Korea's overall exports in the second quarter will rise by about 30% year-on-year.

Sanghyun Park, Senior Specialist at iM Securities, explained, “Unlike previous cycles of high oil prices, the main reason for the KOSPI’s strong rally is the semiconductor trade surplus, which far outweighs the oil trade deficit. Even if high oil prices persist, the scale of the trade surplus could further expand, providing strong upward momentum for our economy and stock market, given the current semiconductor market cycle.”

The super boom in memory semiconductors has further increased the contribution of Samsung Electronics and SK hynix to the KOSPI’s upward trend. According to Meritz Securities, between January and April this year, Samsung Electronics and SK hynix alone accounted for KRW 427 trillion out of the KOSPI’s total profit estimate increase of KRW 472 trillion, which is 90.8%. Their combined share of the KOSPI’s expected net profit for the year is 70.7%, and their combined market capitalization represents 42.2%. From January last year to the end of April this year, the KOSPI rose by 4,241 points-of which Samsung Electronics and SK hynix were responsible for 53% of the gain.

With the favorable semiconductor market conditions expected to continue, further gains for the KOSPI are seen as entirely possible. Both domestic and international securities firms are raising their KOSPI forecasts. Among global investment banks, JP Morgan set its KOSPI target at the 8,500 level last month; Goldman Sachs and Nomura have both forecast 8,000. Among Korean securities firms, Shinhan Investment raised its upper forecast to 8,600, Hana Securities projected 8,470, and Samsung Securities set its target at 8,400.

Foreign Capital Inflow... Expectation to Resolve Korea Discount

Global Investment Banks Raise Targets Continually, Predicting KOSPI 8000

Expansion of AI Infrastructure Benefits in Power, Shipbuilding, and Defense Industries

PER Below 10 Times Compared to Corporate Earnings Perceived as 'Undervalued'

The Memory Semiconductor Bottleneck in the AI Era Is Likely to Intensify

While the semiconductor industry is entering a prolonged boom and record-breaking results are expected, analysis shows that the Korean stock market remains undervalued, suggesting significant room for further gains in the KOSPI.

Shipments of AI servers are up 28% year-on-year, more than double the overall server market growth rate, while memory inventories are at historic lows with only one to two weeks of supply remaining. This supply shortage is expected to drive up DRAM and NAND flash prices by 250% and 187%, respectively, compared to last year.

KB Securities forecasts that the KOSPI’s operating profit this year will hit a record KRW 866 trillion, up 182% from last year, led by Samsung Electronics and SK hynix. The combined operating profit for Samsung Electronics and SK hynix is expected to reach KRW 586 trillion, about five times higher than TSMC’s (KRW 129 trillion), which ranks 11th globally. However, the two Korean companies’ combined market capitalization falls far short of TSMC’s (KRW 2,869 trillion), highlighting the excessive undervaluation compared to performance. Samsung Electronics is projected to achieve KRW 488 trillion in operating profit next year, becoming the world’s number one company in operating profit. SK hynix is also expected to reach KRW 358 trillion in operating profit next year, ranking third globally.

The ripple effects of AI are rapidly spreading beyond semiconductors to the entire industrial ecosystem. In particular, capital expenditures by global big tech companies are projected to reach about $650 billion this year, up more than 70% year-on-year, signifying a fundamental structural shift beyond a simple thematic boom.

In fact, AI-related power infrastructure has come into the spotlight. The explosive expansion of data centers has led to a surge in power demand, making expansion of ultra-high voltage transmission lines and replacement of electrical equipment such as transformers a key growth driver over the medium to long term. Additionally, the machinery and shipbuilding sectors are being highlighted as hidden beneficiaries of AI-related infrastructure investment. Demand for construction and mining equipment is recovering, especially in emerging markets, while the shipbuilding industry is gaining new opportunities as LNG and offshore plant investments expand during the energy transition for AI infrastructure operations.

The defense and financial sectors also serve as major pillars supporting the KOSPI’s fundamental strength. Increased demand for defense due to expanding global geopolitical risks is boosting earnings visibility, while the financial sector is securing both downside stability and profitability thanks to increased stock market trading volume and stronger shareholder return policies.

Overall, the current market is seen as entering a performance-driven rotational rally, with semiconductors as the leading sector and momentum spreading to power infrastructure, machinery, and finance. These broad-based industries, now established as key partners in the AI ecosystem, are each proving their own earnings momentum, driving the KOSPI’s new leap forward.

Capital Market Reforms Have Also Fueled the KOSPI’s Surge

A driving force behind the KOSPI’s record-breaking rally has been the government’s strong efforts to reform the capital market. Institutional reforms have directly targeted chronic issues historically blamed for the “Korea Discount,” such as opaque corporate governance and reckless duplicate listings, serving as a decisive turning point in foreign investor sentiment.

Government Governance Reform, Strengthening Shareholder Return Policies

Credit Balance Surpasses 36 Trillion Won... Signs of Overheating Also Persist

Middle East Risks and Market Concentration, Future Volatility Factors

In particular, three rounds of amendments to the Commercial Act have fundamentally changed the operating principles of the market. In July last year, the “Directors’ Duty of Loyalty to Shareholders” was expanded from “the company” to “the company and shareholders,” legally requiring management to prioritize the interests of minority shareholders, not just controlling shareholders. In August, mandatory cumulative voting and separate election of audit committee members were broadened for large listed companies. This February, a law was enacted mandating that treasury shares acquired by a company must be retired within one year.

These institutional reforms have not remained mere slogans but have led to increased dividends and active shareholder return policies. This has provided strong momentum for a massive influx of global capital into the Korean market, which had previously had one of the world’s lowest valuations. Government-led regulatory reforms, combined with robust semiconductor earnings, have served as the key driver that pulled the KOSPI out of its undervaluation trap.

Shadow Side of the Rally: Increased Margin Trading and Semiconductor Concentration

Experts point out that while the KOSPI remains undervalued relative to earnings, there is ample room for further gains based on sector-specific earnings momentum.

Hyoseop Lee, Research Fellow at the Korea Capital Market Institute, said, “Looking at the KOSPI’s forward price-earnings ratio (PER), it is still below 10 times, and with such strong performance in semiconductors, defense, and shipbuilding, there remains upside potential from a valuation perspective. U.S. tech stocks continue to see upward revisions in earnings forecasts, and compared to global peers like Micron and TSMC, Korean semiconductor firms remain undervalued.” He added, “Real estate in Korea is still highly attractive, and policies such as strengthening the stewardship code, tightening delisting criteria, and improving the financial tax system should be pursued over the long term to encourage money movement into the market.”

Jihwan Yang, Head of Research at Daishin Securities, commented, “Major companies reported stronger-than-expected first-quarter results, and expectations surrounding a ceasefire have been reflected in the market. Even after surpassing 7,000 points, the PER remains around 8 times, and with profit estimates being revised upward, the view that the market is undervalued is spreading.” He continued, “The market expects the Middle East situation to be resolved by the third week of this month, but if not, the market could face a correction. Since there was a sharp drop and quick rebound in March, investors should be cautious about stocks that have risen without solid earnings support and focus on large-cap stocks in electronics, securities, and finance.”

However, there are also shadows behind the rapid ascent. The amount of margin trading (“bittoo,” or credit loans) has increased sharply due to the surge in the index, and the concentration of momentum in specific themes or large-cap stocks could further heighten market volatility. According to the Korea Financial Investment Association, as of April 29, the balance of domestic margin loans stood at KRW 36.0682 trillion, surpassing KRW 36 trillion for the first time. The credit balance has risen 31.54% in just four months, from KRW 27.4207 trillion at the start of the year.

-

Reporter Lim Chunhan choon@asiae.co.kr

-

Reporter Lee Changhwan goldfish@asiae.co.kr

-

Edit Kang Dongwon kangdw76@asiae.co.kr

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![[Culture Interview] "Unifying the Fragmented Music Market... Super Fans Are the Next Competitive Edge"](https://cwcontent.asiae.co.kr/asiaresize/304/2026042817051344090_1777363513.jpg)