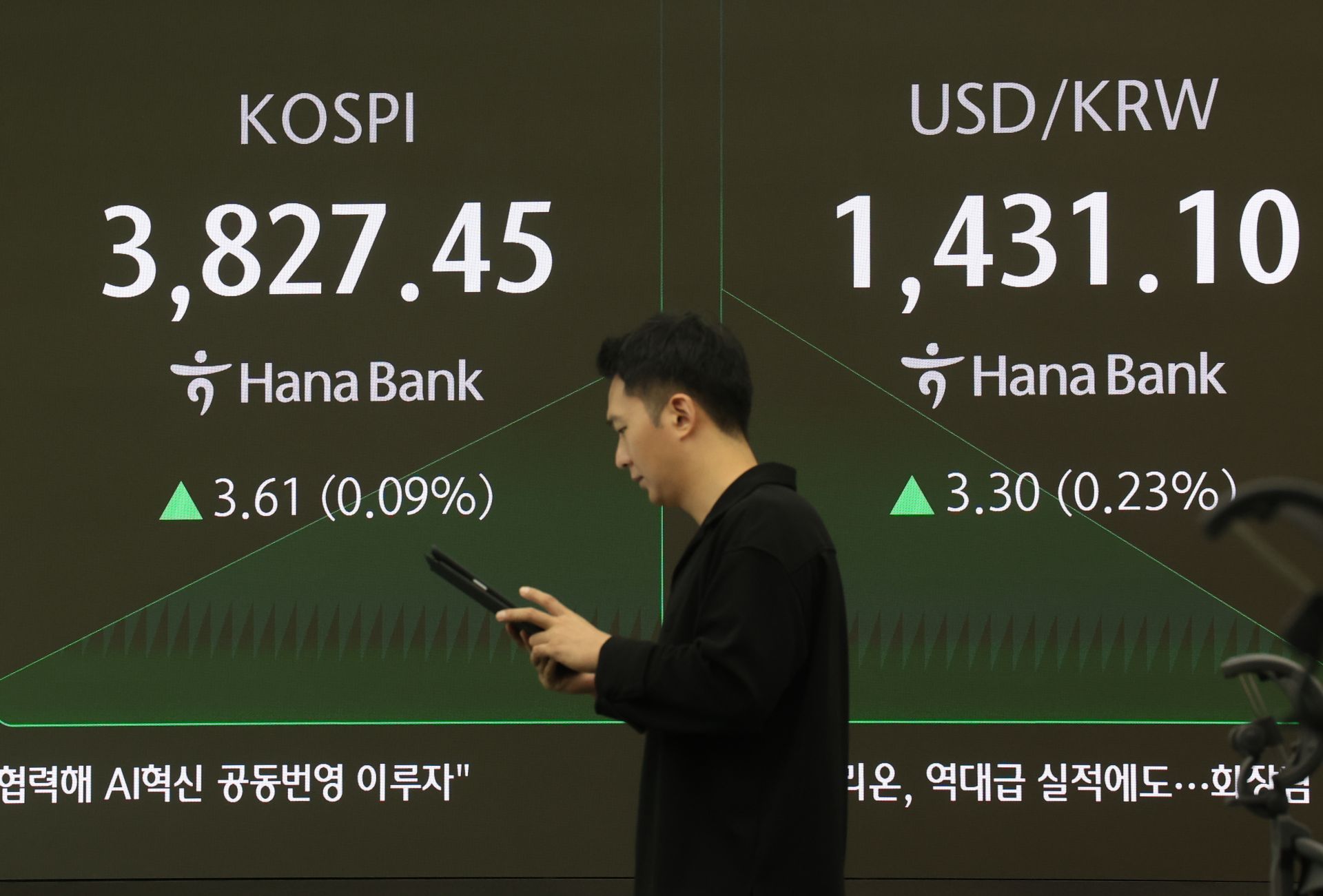

KOSPI up about 60% since the beginning of the year

Buffett Indicator shows 'Overheating Warning'

Some voices raise concerns about a bubble

Buffett Indicator shows 'Overheating Warning'

Some voices raise concerns about a bubble

by Song Hwajung

by Kim Jinyeong

by Choi Yujeong

Published 22 Oct.2025 14:19(KST)

The KOSPI continues its record-breaking rally. Earlier this month, the KOSPI surpassed the 3,500 mark for the first time in history, and has since broken through 3,600, 3,700, and even 3,800, maintaining an unstoppable upward trend. As the KOSPI rises at a rapid pace, concerns about a potential bubble are also growing. However, experts agree that the current situation is different from the dot-com bubble or the COVID-19 era, and that it cannot yet be considered a bubble. With improved earnings and policy enhancements, some predict that the bullish market will continue into next year.

As the KOSPI continues to hit all-time highs almost daily, there are increasing voices expressing concerns about a bubble. Some point out that the current phenomenon, where any stock related to artificial intelligence (AI) attracts strong buying interest, resembles the stock market during the dot-com bubble period (1999-2000). The KOSPI, which has risen by nearly 60% since the start of the year, has already surpassed the 1998 growth rate (49.93%) and is rapidly closing in on the 1999 record (82.78%). Considering that the KOSPI plunged by 50% in 2000, the year after the dot-com bubble burst, it is understandable that investors are becoming increasingly cautious.

There are various factors fueling concerns about a market bubble. In the United States, where the AI bubble debate emerged earlier than in Korea, the share of IT hardware, software, and research & development (R&D) in nominal GDP reached 7.16% in the second quarter of this year, surpassing the 6.25% recorded in the first quarter of 2000 at the end of the dot-com bubble. As of October 10, the price-to-earnings ratio (PER) of the top 1,000 companies by market capitalization listed on the US stock market stood at 27.1 times, higher than the 26.2 times at the peak of the bubble in late February 2000.

Market anxiety is also evident in quantitative indicators. The "Shiller Index" (CAPE), which shows the current price level relative to the average real (inflation-adjusted) earnings per share over the past 10 years, reached 40.21 as of October 21, the highest since the dot-com bubble in December 1999 (44.19). This index, devised by Nobel laureate Robert Shiller of Yale University, indicates that the higher the value, the more overheated the stock market is compared to the economy and corporate earnings.

The "Buffett Indicator" has also flashed an overheating warning. This indicator is the ratio of a country's total stock market capitalization to its nominal GDP. Generally, a value below 80% is considered undervalued, 80-100% is fair value, and above 100% is overvalued. At the peak of the dot-com bubble in 2000, the US Buffett Indicator soared to the 140% range; as of October 20 (local time), it exceeded 220%. In Korea, it also reached an all-time high of 125% as of October 21.

Despite growing bubble concerns, stock market experts believe that the Korean stock market is not in a bubble. Yoon Changyong, head of the Research Center at Shinhan Investment Corp., said, "I do not see this as a bubble. While there may be some short-term valuation pressure, the overall rise in stock prices is based on earnings improvement and changes in industrial structure," adding, "Earnings improvements are clearly visible, and the overall market PER is still below 12 times, making it hard to call this overheating. In particular, as earnings estimates for key sectors such as semiconductors and secondary batteries are being revised upward, this is an earnings-based rally, which is fundamentally different from a simple liquidity-driven rally."

Some, however, believe the bubble is growing. Kim Dongwon, head of Research at KB Securities, stated, "I believe we are in a phase where the bubble is expanding," noting, "The S&P 500's valuation has reached its highest level since the dot-com bubble, the proportion of stocks in US household financial assets is at an all-time high, and the share of US stocks owned by foreigners is the highest since 1969."

There is also analysis that the situation in the US and Korea is different. In the US, bubble concerns are rising because excessively optimistic projections about artificial intelligence (AI) are reflected in tech stocks, but for Korean semiconductor companies, the rally is based on actual demand, making it hard to call it a bubble. Lee Kyungmin, head of FICC Research at Daishin Securities, said, "While there are bubble concerns centered on US AI tech stocks, it is difficult to say that the KOSPI and the semiconductor sector, which is leading the recent rally in the domestic market, are in bubble territory," adding, "The fundamental reason for bubble concerns in the US stock market is that investment by major AI-related companies may be excessive compared to potential demand, and that overly optimistic forecasts about the potential growth of the AI market are being reflected in the stock prices of tech and infrastructure companies leading the market to all-time highs. The current PER of the S&P 500 tech sector is 43 times, with a forward PER of 28 times, while Nvidia, which is driving the AI momentum, has a PER of 52 times and a forward PER of 28.3 times. These stock prices, which have already priced in high expectations, suggest that we may be at the early stage of a bubble." He continued, "In contrast, the stock prices of semiconductor and infrastructure sectors leading the domestic market are based on the actual infrastructure investment targets of downstream companies, the government, and institutions, as well as realistic expectations for the AI services market. Actual infrastructure investments are being made, leading to supply shortages in semiconductors and electrical equipment, and rising DRAM prices."

There is also the view that, in terms of valuation, it is difficult to call the current situation a bubble. Yoo Jongwoo, head of Research at Korea Investment & Securities, said, "From a valuation perspective, the market is more stable compared to the liquidity bubble in 2021," pointing out, "As of October 17, the KOSPI's 12-month forward PER is 11.3 times. During the liquidity-driven rally following the COVID-19 outbreak in 2020, the KOSPI's 12-month forward PER once rose to 14.6 times."

Experts believe that the current market is different from the liquidity-driven rallies seen during the dot-com bubble or the COVID-19 era. Currently, the rally is supported by actual earnings, and there are no warning signs typical of bubbles, such as sharp rises in theme stocks lacking fundamentals or excessive corporate investment.

Kim Yonggu, head of Investment Strategy at Yuanta Securities, said, "The S&P 500's 12-month forward PER is now 23.0 times, close to the 24.5 times peak during the dot-com bubble in 2000, so it is clear that both domestic and global stock markets are at valuations and price levels that could intensify the bubble debate." He added, "However, the current market leaders-AI and hyperscaler blue chips such as Microsoft, Meta, Amazon, Google, and Oracle-are all continuing to expand their capital expenditures and free cash flow, and unlike during the dot-com bubble, there is no fundraising through stock issuance or borrowing. The current AI supercycle is being driven by organic cash flow and profitability." He further explained, "The AI data center capital expenditure supercycle is likely to be further boosted by government fiscal policy and preemptive monetary easing (rate cuts), which will, in turn, be reflected in improved semiconductor industry conditions and additional improvements in Korea's exports and earnings."

Lee Younggon, head of Research at Toss Securities, said, "The growth of the AI industry is accompanied by real investment and earnings support, unlike during the dot-com bubble," adding, "Stock prices are not rising solely on future growth expectations, but as part of a virtuous cycle driven by actual profit generation and investment."

There is also analysis that this bull market is driven by changes in industrial structure, making it different from past bubbles. Yoon Changyong said, "Whereas past bubbles were formed by expectations and liquidity, the current phase is driven by industrial restructuring and real investment expansion. The value chain is expanding from intermediate goods to finished goods and services, and global companies are clearly moving to expand capital expenditures and secure technological standards. The existence of real growth momentum differentiates the current market from the past." Cho Suhong, head of Research at NH Investment & Securities, said, "This rally is not a forced rise due to liquidity, but rather the result of structural polarization serving as the market's fundamental driving force. Industries with high time efficiency and technological intensity are generating excess profits, while traditional manufacturing and domestic sectors are stagnating. In other words, this is a transition from a simple liquidity-driven rally to a productivity-driven rally."

Some predict that the AI industry is entering the early phase of a bubble. Cho said, "In terms of stock price growth, the AI industry is now entering the initial stage of a bubble, as AI-related stocks are responding more to news than to actual earnings and are rising continuously without corrections." However, he also noted that it will take considerable time before the AI bubble bursts, as demand remains strong. Cho added, "Ongoing shortages in AI hardware supply due to expanding AI demand suggest that it will take a significant amount of time before the AI bubble bursts."

Park Heechan, head of Research at Mirae Asset Securities, said, "As bubble theories related to US AI investment are being raised, it will be especially important to closely monitor this trend next year."

The bullish trend in the stock market is expected to continue into next year. Yoo Jongwoo said, "The stock market rally is likely to continue next year, as improving earnings and tax reforms enhance the attractiveness of equities, accelerating the shift of capital from other assets into stocks."

Song Hwajung pancake@asiae.co.kr

Kim Jinyeong camp@asiae.co.kr

Choi Yujeong yjchoi@asiae.co.kr

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.